Definition

Charging as a Service (CaaS) is a business model for electric vehicle (EV) charging infrastructure in which a third-party service provider owns, installs, operates, and maintains charging equipment on behalf of a customer. The customer — typically a fleet operator, property owner, municipality, or employer — pays recurring fees (subscription, usage-based, or revenue-share) rather than making upfront capital expenditures on hardware and installation. CaaS is conceptually analogous to Software as a Service (SaaS): the customer consumes a service without owning or managing the underlying physical assets.

On This Page

Historical Context & Market Growth

CaaS emerged as a response to the same friction that slowed early cloud computing adoption: high upfront cost, technical complexity, and the risk of backing the wrong technology. EV charging hardware presents similar barriers — a commercial Level 2 charger costs $2,000–$7,000 before installation, while a DC fast charger can exceed $50,000–$150,000 installed, not counting grid connection upgrades that can run into the hundreds of thousands.

The model gained traction in the early 2020s alongside accelerating EV adoption and the emergence of large-scale fleet electrification commitments. The 2021 US Infrastructure Investment and Jobs Act (which funded the NEVI program) and the EU Alternative Fuels Infrastructure Regulation (AFIR) created regulatory tailwinds that made multi-year CaaS contracts — with defined performance standards — an attractive risk structure for both operators and infrastructure investors.

Market Size

CaaS market estimates vary significantly across research firms depending on scope — some include only pure-play managed service contracts; others bundle all networked charging revenue. Grand View Research, one of the most cited sources, estimates the narrowly defined CaaS market at $406.5 million in 2025, reaching $2.9 billion by 2033 at a CAGR of approximately 28.6%. Broader “EV charging services” markets that include network fees and energy management reach different figures. The data below reflects the Grand View Research CaaS-specific estimate.[1]

Regional Distribution (2025)

| Region | Market Position | Key Drivers |

|---|---|---|

| Asia Pacific | Largest region — ~31% share (2025) | China’s dominant public charging build-out; government subsidy programs; rapid EV penetration |

| Europe | ~29% share; fastest growing | AFIR mandates, strong EV penetration (Norway >80% new car sales), corporate net-zero commitments |

| North America | ~22% share (2024) | NEVI program infrastructure spending, fleet electrification mandates (California ZEV rules), growing CPaaS adoption |

| Middle East & Africa | Emerging; UAE highest CAGR projected | Government EV mandates in UAE, Saudi Arabia; tourism and hospitality sector demand |

CaaS vs. Traditional Ownership Models

The fundamental difference between CaaS and conventional charging deployment is who owns the asset and who bears the risk. In traditional deployment, the site host is also the asset owner — capital expenditure, technology obsolescence, maintenance cost, and uptime risk all fall on the customer. CaaS inverts this structure.

| Dimension | Traditional Ownership | Charging as a Service (CaaS) |

|---|---|---|

| Capital expenditure | Customer bears full upfront cost (hardware, installation, grid upgrades) | Provider bears CapEx; customer pays monthly OpEx |

| Asset ownership | Customer owns the charging equipment | Provider retains equipment ownership throughout contract |

| Operations & maintenance | Customer responsible — or contracted separately at additional cost | Included in service; provider handles preventive and corrective maintenance |

| Technology obsolescence risk | Customer bears risk; hardware may need replacement as standards evolve | Provider bears risk; upgrades often included in contract terms |

| Uptime guarantee | Not standard; dependent on vendor support response times | SLA typically included (e.g., 95–99% uptime) |

| Software / platform | Separate licensing cost; customer manages integration | CPMS included; provider manages all software updates |

| Contract structure | One-time purchase; ongoing O&M contracts separate | Multi-year agreement (typically 3–7 years) |

| Balance sheet treatment | Capital asset (depreciated) | Operating expense (off-balance-sheet, depending on accounting treatment) |

| Scalability | Requires new capital approval for each expansion | Contract modifications; provider handles procurement and installation of additional units |

The CapEx-to-OpEx shift is the most cited driver of CaaS adoption among fleet operators and property owners. However, the total cost over a CaaS contract term is typically higher than equivalent outright ownership — the premium reflects the value of transferred risk (uptime, maintenance, technology), predictable budgeting, and reduced management overhead. Neither model is universally superior; the optimal choice depends on capital availability, technical capacity, and risk tolerance.

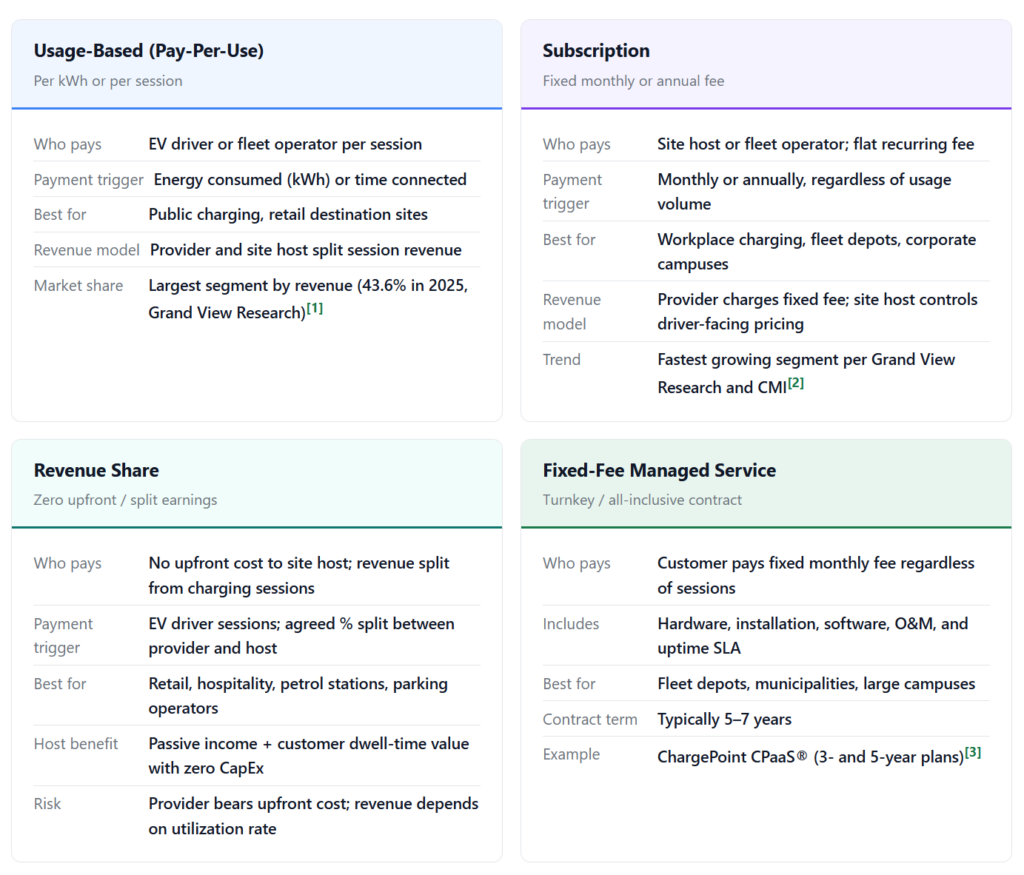

Business Model Types

CaaS encompasses several distinct commercial arrangements. In practice, providers often offer a portfolio of models to serve different customer types.

| Usage-Based (Pay-Per-Use) | Subscription | Revenue Share | Fixed-Fee Managed Service | |

| Who pays | ||||

| Payment trigger | ||||

| Best for | ||||

| Revenue model | ||||

| Market share |

Financed / Hybrid Model

A variant that sits between outright purchase and pure CaaS: the customer finances the hardware purchase through a third-party lender (e.g., Goldman Sachs Renewable Power partnered with ChargePoint for this in 2022[4]), then pays down the asset over time while the provider handles software and O&M under a separate service agreement. This preserves some ownership benefits while reducing upfront cash outlay.

Service Lifecycle

A CaaS engagement typically follows a structured multi-phase process from initial assessment through ongoing operations. The provider bears project management responsibility across all phases.

Site & Demand Assessment

Evaluation of parking layout, existing electrical capacity, transformer proximity, and utility access. For fleet customers: analysis of vehicle duty cycles, dwell time, and charging behavior to right-size the charging solution.

Solution Design & Commercial Structure

Selection of charger types (AC Level 2 vs. DC fast), power levels, and load management strategy. Commercial model definition: pricing structure, contract term, revenue share percentages, and uptime SLA. Optional integration of solar PV or battery storage for energy optimization.

Permitting & Utility Coordination

Provider manages building permits, AHJ approvals, and utility interconnection applications. Identification and application for applicable federal, state, or local incentive programs (NEVI funding, state grants, utility rebates).

Installation & Commissioning

Civil works, electrical upgrades, charger installation, and network configuration. Provider manages subcontractor selection and construction oversight. Site goes live only after passing safety, performance, and compliance checks.

Ongoing Operations, Monitoring & Support

Provider monitors charger uptime 24/7 through CPMS; handles both preventive and corrective maintenance. Manages software platform for billing, driver support, and energy management. SLA performance is tracked and reported to the customer.

Scaling & Technology Refresh

Contract modifications to add charging capacity at existing or new sites. Technology refresh provisions allow hardware upgrades as charging standards evolve (connector types, power levels, OCPP version upgrades) without customer-facing capital decisions.

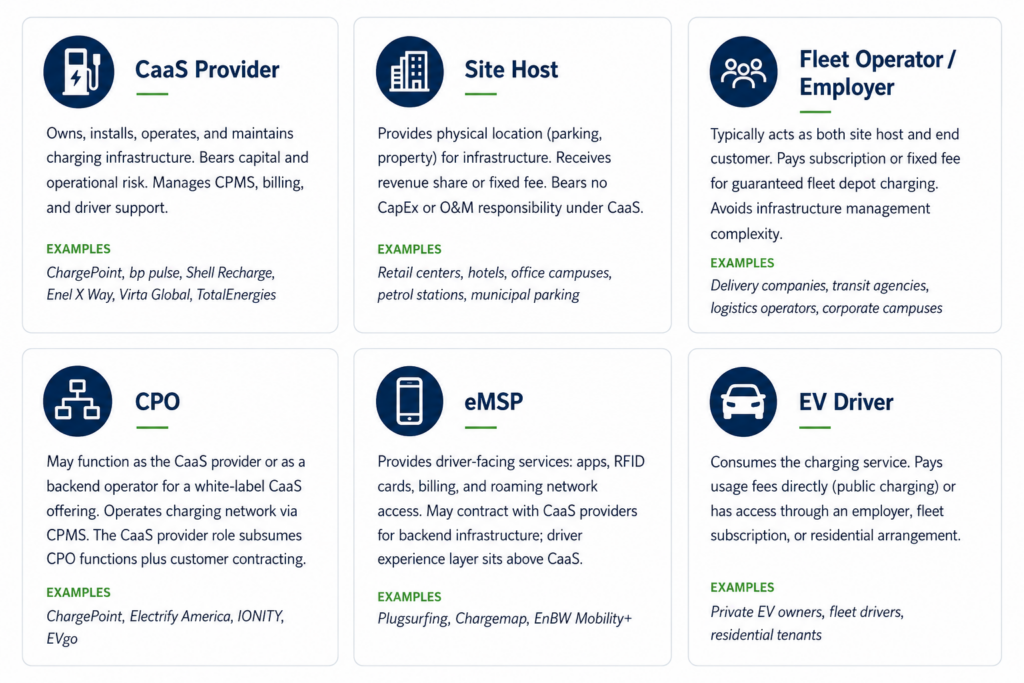

Stakeholders & Roles

The CaaS ecosystem involves five distinct actors with different responsibilities, risk exposures, and commercial interests.

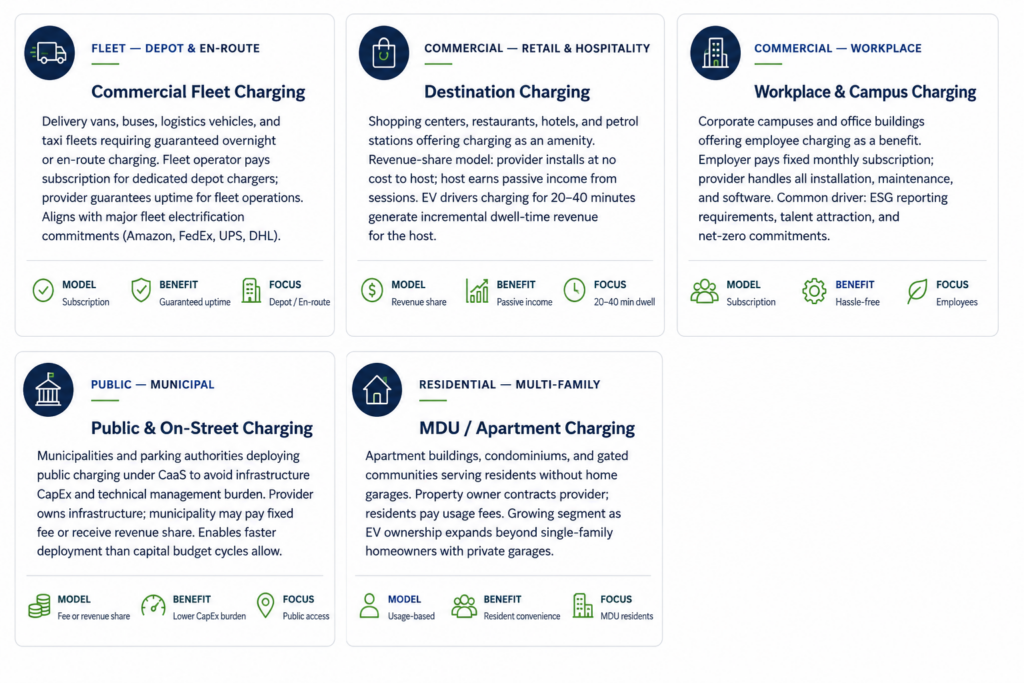

Applications & Use Cases

CaaS is deployed across five major market segments, each with distinct commercial structures and value propositions.

By application, the commercial segment accounts for approximately 83% of the CaaS market, with residential at ~17%. By charging point type, AC Level 2 charging currently holds the largest installed base under CaaS contracts, while DC fast charging holds a smaller share of installations but a disproportionate share of revenue per charger due to higher session fees.[1]

Key Industry Players

| Company | Geography | CaaS Offering |

|---|---|---|

| ChargePoint (CHPT) | Global | ChargePoint as a Service® (CPaaS®) — 3- and 5-year subscription plans covering hardware, software, installation, and O&M. Provider retains hardware ownership. Partnered with Goldman Sachs Renewable Power to offer financed options.[3][4] |

| bp pulse | Global | End-to-end CaaS structured in four phases: Design, Deploy, Operate (proprietary “Omega” CSMS), and Maintain (“Elevate” program). Active in UK, Europe, and US. |

| Shell Recharge Solutions | Global | Managed charging services for fleets and commercial properties. Combines Shell’s global footprint with acquired charging network assets. Active in EU, US, and APAC. |

| Enel X Way | Europe / US | Fixed-fee managed service model: no upfront cost, 5–7-year contract terms, 99% uptime SLA. Hardware, software, installation, and maintenance bundled. |

| TotalEnergies | Europe / Global | Integrated EV charging solutions; plan to equip 500+ service stations across Europe. CaaS offerings bundled with energy supply contracts for fleet customers. |

| Virta Global | Platform | White-label CPMS platform managing 120,000+ chargers across 35+ countries. Enables partners (CPOs, utilities, OEMs) to deliver CaaS under their own brand. |

| Tesla | Global | Operates the Supercharger network (now open to non-Tesla EVs via J3400 adapters and NACS ports). Destination Charging Program offers revenue-share for hotel/retail site hosts at no hardware cost. |

| Electrify America | US / Canada | Announced commitment to 10,000+ new DC fast chargers by 2026. Primarily public DC fast charging; Electrify Commercial serves fleet CaaS contracts. |

“CPaaS democratizes EV charging by bringing all of the benefits of the ‘as a Service’ pricing model to businesses interested in providing comprehensive EV charging solutions without purchasing them outright.”— ChargePoint, ChargePoint as a Service® product description[3]

Adjacent & Related Business Models

CaaS is often confused with adjacent models that share some characteristics but differ in scope, ownership structure, or responsibilities.

| Model | Distinction from CaaS |

|---|---|

| Charge Point Operator (CPO) | CPOs operate charging networks but may not own the hardware or offer bundled service contracts to site hosts. CaaS is a superset: it adds customer contracting, site host agreements, and asset ownership to CPO functions. |

| CPO-as-a-Service | A subset of CaaS focusing specifically on management and optimization of existing infrastructure owned by the customer. The provider does not own the hardware. Scope is software and operations only. |

| Equipment Leasing | Customer leases hardware but retains operational responsibility — O&M, software, uptime are not included. The customer bears operational risk; CaaS does not. Leasing converts CapEx to a financing cost rather than an outsourced service. |

| White-label CaaS | The CaaS provider supplies hardware, software, and full operations; a third party (automaker, utility, retail brand) brands the charging service under their own name. The underlying service structure is CaaS; only the customer-facing brand changes. |

| Managed Energy Services (MESS) | Broader services agreements covering total energy management for a facility — including solar PV, BESS, building HVAC, and EV charging as one integrated service. CaaS is a subset when charging is included in these arrangements. |

Relationship to the EV Charging Ecosystem

CaaS is a business model layer, not a technical standard. It relies on the technical standards and hardware components of the broader EV charging ecosystem to function.

| Component | Relationship to CaaS |

|---|---|

| EVSE (Hardware) | CaaS providers procure and own the physical EVSE. Hardware selection determines charging speed, connector compatibility, and total cost basis for the service. The customer never holds title to the equipment under a pure CaaS contract. |

| CPMS (Software) | The Charging Station Management System is what makes CaaS operationally viable at scale — it enables remote monitoring, OTA firmware updates, billing, load management, and SLA reporting across large networks without on-site staffing. |

| OCPP | CaaS providers that manage multi-vendor hardware portfolios depend on OCPP interoperability. OCPP 2.0.1 — now an IEC standard — allows a single CPMS to manage chargers from different manufacturers. Without OCPP, each hardware brand would require separate management software. |

| BESS (Battery Storage) | CaaS packages increasingly include BESS to enable peak demand management and reduce demand charges at DC fast charging sites. The provider bears the BESS capital cost under a CaaS contract, bundling storage economics into the service fee. |

| V2G / Bidirectional Charging | Emerging CaaS offerings include V2G capability, enabling providers to participate in grid services markets (frequency regulation, demand response) using aggregated fleet battery capacity. Revenue from grid services can subsidize lower service fees for customers. |

| OCPI (Roaming) | CaaS providers with public-facing networks use OCPI to enable EV driver roaming across partner networks, improving utilization of their deployed assets and increasing revenue per charger. |

Joint’s hardware and software stack supports CaaS deployment models for distributor and CPO partners. The OCPP 2.0.1-certified EVM, EVH, and EVD series, combined with the MPO white-label CPMS platform, give partners the technical foundation to deliver CaaS without developing proprietary software. JointCharging’s AI Doctor platform (targeting 99% uptime, Q2 2026) directly supports the uptime SLA commitments that CaaS contracts require. Hardware manufactured at Xiamen and Malaysian facilities provides supply chain options for CaaS operators serving North American and European markets.

See Also

- EV Charging Glossary

- CPO (Charge Point Operator)

- DC fast charging (DCFC)

- Open Charge Point Protocol (OCPP)

- Battery Energy Storage System (BESS)

Sources & References

- [1] Grand View Research, “Charging As A Service Market Size, Share & Trends Analysis Report,” 2025/2026. grandviewresearch.com

- [2] Coherent Market Insights, “Charging as a Service Market Size, Share & Forecast to 2032,” 2025. coherentmarketinsights.com

- [3] ChargePoint, “ChargePoint as a Service® (CPaaS®): Subscribe to the Future of EV Charging.” chargepoint.com; ChargePoint Fleet Electrification Services. chargepoint.com/fleet/services

- [4] ChargePoint, “ChargePoint Partners with Goldman Sachs Renewable Power to Offer New Customer Solutions,” March 29, 2022. chargepoint.com

- [5] MarketsandMarkets, “Charging as a Service Market 2025–2035,” projected CAGR 29.1%, 2025–2035. marketsandmarkets.com

- [6] GII Research / Grand View Research, “Charging As A Service Market,” subscription segment growth data, 2026. giiresearch.com